Blog

Enterprise Software in a Remote World: COVID-19's Continued Impact on Business

by Alex SharataSep 30, 2020

At the end of Q1, we shared some initial hypotheses about the impacts the global pandemic would have on enterprise software companies. Fast forward through Q2, and many of our initial impressions around COVID-19’s impact have held true. Still, the impact has been far from uniform across company sectors and stages. We’ve seen a wide range of approaches to adjusting sales tactics, moderating spend, and keeping teams motivated. To better gauge these company responses, we recently conducted a survey across our enterprise software portfolio and compared and contrasted the findings with reports from public SaaS counterparts. We hope this data will be useful to operators leading teams through this challenging time.

Five core themes encapsulate our findings:

Base expectations around the response to COVID-19 held true

~50% of businesses were on a path to recovery by the end of Q2

All companies looked to conserve cash; Developer tools, cloud infrastructure and S&M software were the most impacted by reductions in software spend

Companies entered a challenging new selling environment with smaller S&M teams and constricted budgets from buyers - new sales techniques were explored but with mixed results.

Companies prioritized culture and individual engagement to keep morale high, and relied more heavily on OKRs to keep teams operating efficiently while at home

This is the second post in our series on the enterprise response to COVID. Click here for Q1 findings.

1. Base expectations around the response to COVID-19 held true.

Video and chat software providers were the biggest beneficiaries of the work from home transition. Nearly 60% of companies surveyed increased their spend on this category of software, and 40% maintained existing spend. Productivity tools and customer success software similarly saw negligible declines in software spend, though only 30% and 13% of companies increased their spend within these areas, respectively.

Enterprise buyers proved to be more resilient. Companies serving SMBs with less than $50K ACVs performed worse overall relative to plan versus companies serving up-market, enterprise customers. In fact, 100% of the companies that expect to end the year on or above their pre-COVID-19 plan and without COVID-19-induced tailwinds had $100K+ ACVs.

While a majority of companies (57%) experienced heightened difficulty closing sales in a remote environment, a severe shift was only felt by 1 in 10. Over a quarter of companies reported that the sales motion felt ‘about the same’ as pre-COVID-19.

In examining the impact to specific verticals, we found that travel, government, and retail were the hardest hit end markets, while financial services and tech were relatively insulated.

2. ~50% of businesses were on a path to recovery by the end of Q2.

We started to see a bifurcation in expected rest-of-year performance. In comparing estimated CY20 performance with Q1 and Q2 performance, we noted that 48% of businesses started—and expect to continue—to see gains towards their pre-COVID-19 plan through the end of the year. 52% of businesses, however, expect that tough quarters will continue and are planning for similar or slightly worse performance in Q3 and Q4.

A few anonymous quotes from within our portfolio detail how growth trajectories are beginning to normalize in the back half of the year:

“In some ways, the numbers look like we were on pause for 3 to 4 months and are now back to growing. In other words, imagine taking the 2020 plan and having it start in May instead of January.”

“Material slowdown in customer acquisition and cohort revenue growth in March and April. Normal activity has resumed in May to August.”

“Recovery is slightly faster than we anticipated in April...we are now finally getting ahead of our post-COVID plan from April.”

3. Changes in company spend were surprising: developer tools, cloud infrastructure, and sales and marketing tools were the most impacted by reductions in software spend.

All companies looked to conserve cash at the start of the pandemic, and we expect a focus on efficiency to continue. Still, areas of impact were not uniform, and we believe there was a slight correlation with company trajectory. Generally, we saw that companies with a deteriorating RoY outlook reigned in spend on developer tools and cloud infrastructure. Companies on a positive trajectory reduced expenditure on sales and marketing tools.

As a category, developer tools saw the largest reduction of investment, with 22% of all participants decreasing spend. While there are many possible explanations for this trend, given the recent proliferation of such tools with individual developers as buyers today, it is likely there was some consolidation where those tools lacking sufficient bottoms-up adoption were turned off. Many tools in this category are built on open source frameworks, and companies may have also opted to revert back to a purely open source version of the technology to maintain in-house.

Separately, we also saw some tightening in spend on cloud infrastructure. While companies may have been impacted by declining customer traffic and volume, we expect this was more likely due to a concentrated push to renegotiate existing contracts and more aggressively seek discounts with the large providers. Further, as cloud spend is typically pay-as-you-go and less encumbered by long term contracts, it's a natural target for CFOs. This trend was mirrored by public company counterparts. On their earnings call, Datadog mentioned: “customers with large cloud deals from AWS, Azure or GCP look for short-term savings. Note that this is not a new motion as we see many enterprises go through these optimization exercises on a regular basis. What was unusual this quarter was to see a large number of companies going through it at the same time.”

For companies where COVID-19’s impact was less severe in Q2 onwards, S&M tools were the most impacted: 25% of companies trending positively post Q2 still reduced sales & marketing expenditure. We initially hypothesized that customer success software would experience COVID-19 tailwinds and become increasingly important in a remote environment as companies went on the offensive to prevent churn; however, customer success software saw the least amount of incremental investment, with only 13% of participants increasing spend and 78% keeping spend flat.

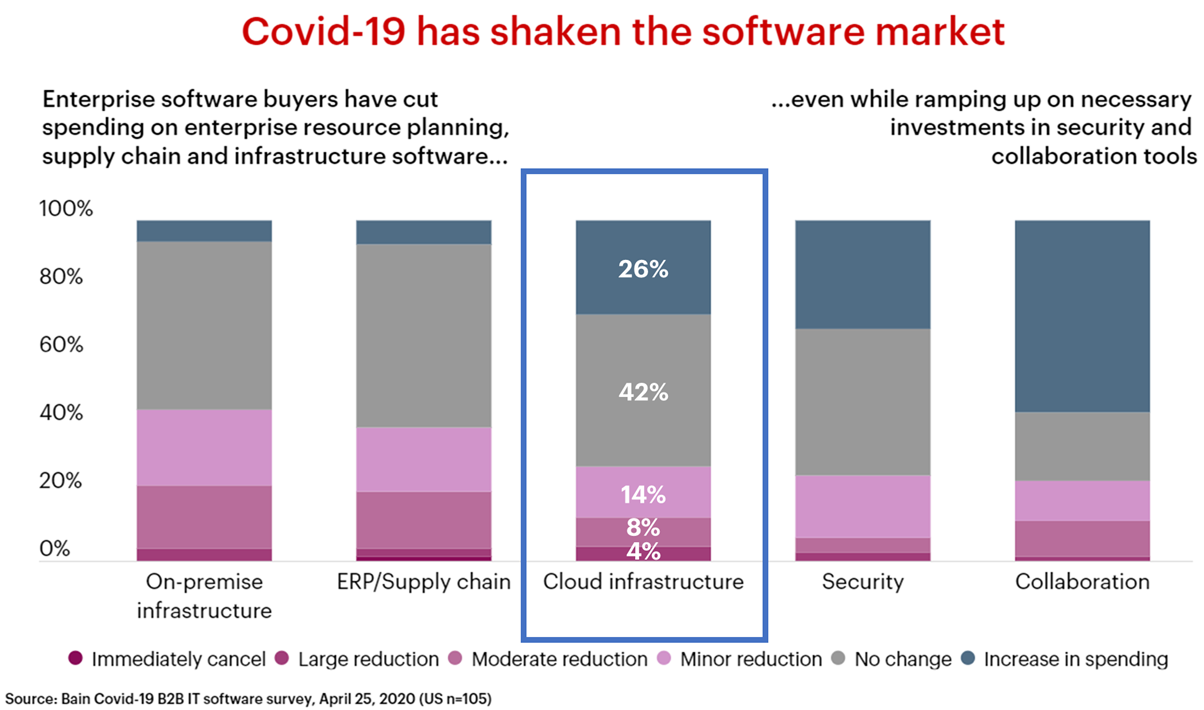

In a recent Bain & Company software survey, more than 50% of buyers said they had already cut their overall software budgets. “Among software categories, some are emerging as priorities that warrant additional spending, especially collaboration and security, as more employees work from home during lockdowns. However, buyers are putting off purchases where they can, including application software suites like analytics, enterprise resource management and customer relationship management.” 26% of respondents to Bain’s survey reduced cloud infra spend while 42% of participants held spend constant.

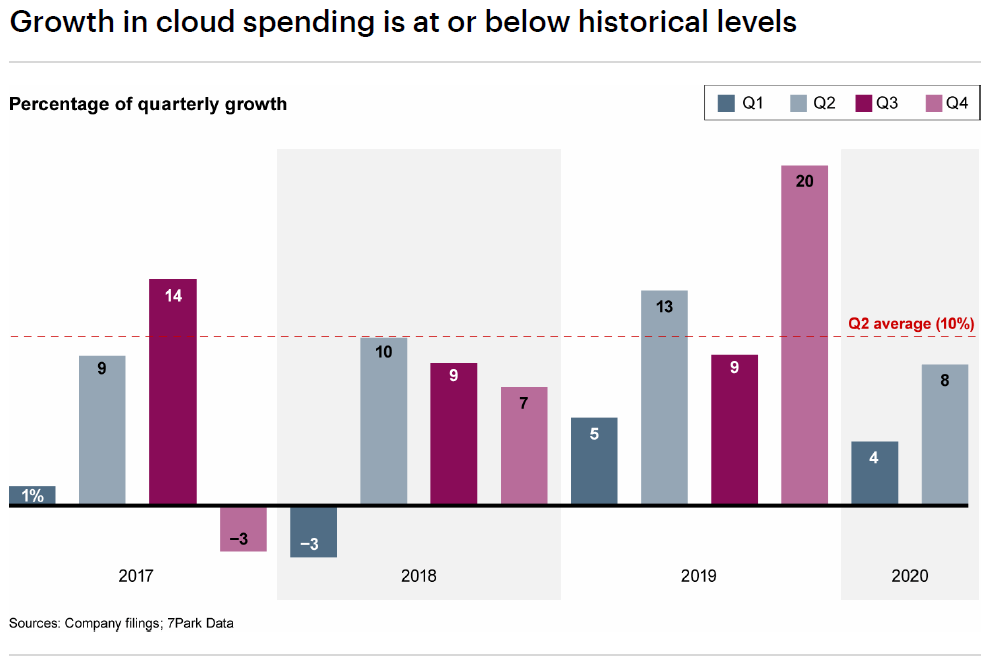

In a separate analysis, Bain found that Q1 2020 cloud spending growth was just a bit lower YoY, but the Q2 2020 growth rate was 5 points lower YoY(figure below). The team shared: “while it’s true that some categories have boomed and a few companies have experienced tremendous growth...overall cloud spending hasn’t grown abnormally.”

Similarly, we believe that interest in video, chat, and productivity software has been decelerating in Q3. While our survey data shows that these sectors managed to avoid budget cuts and have seen absolute growth since the start of the year, comScore data for August 2020 demonstrates that most platforms have seen decelerating unique visitor YoY growth rates. Dropbox’s unique visitor growth rate decelerated to -16% YoY in August from -10% in July, Slack dropped to -14% from flat growth in July, RingCentral’s visitor growth dropped to +50% from 67% in July. As one of few companies bucking the trend, Zoom’s unique visitor growth accelerated to +752% from +661% in July.

Overall, Bain found that 75% of CIOs said that their day-to-day IT operations were not materially impacted by COVID-19. This lines up with our own survey findings where 50% of respondents on average did not make significant changes to their IT stacks or shift spend around as a result of COVID.

4. Companies entered a challenging new selling environment with smaller S&M teams and constricted budgets from buyers—new sales techniques were explored but with mixed results.

With internal and external constraints, companies encountered meaningful headwinds when shifting to fully-remote sales. Nearly 50% of companies reduced their sales and marketing headcount and several also saw customer purchasing budgets shrink. Specifically, 54% of companies with less than $50K ACVs said it’s harder to close business while remote, and 30% of them were under pressure due to budget contractions. Below is a table showing which functional groups expanded or contracted.

For the companies where sales were ‘somewhat easier,’ 50% were in categories that directly benefited from COVID-19. The remaining 50% prioritized executive sponsorship, and were able to get company management involved in more meetings as travel wasn’t necessary. They also saw benefits from cold calling and quickly adapting to hosting a higher mix of virtual events and conferences, which, in some instances, generated more top-of-funnel leads than before due to the lower friction of attending an event online versus in-person. Last, companies continued to tailor messaging around how their products could drive benefits in a remote-first environment.

A few specific quotes from across our portfolio:

Evident ID mentioned, “We have focused on customer education early in the funnel, and we are hitting cost savings hard as deals mature.”

Forethought continued to lean on a largely outbound sales motion, though noticed that cold outreach was initially more difficult with customers away from their desks. They mentioned “things are starting to return back to normal, but we will likely invest in more inbound and marketing-led sales too.”

Logikcull is “using marketing to drive customers to our platform and then relying on a self-sign up / pay-as-you-go model, which gives customers the freedom to use the product as needed without signing annual subscription contracts.”

Splashtop tailored messaging to “focus on specific usage (WFH, hybrid learning, & verticals)."

Conviva found “high quality industry reports like State of Streaming” to be effective in getting the word out.

When reviewing public earnings, we found that our portfolio company founders were experiencing the same selling challenges as public SaaS businesses.

Slack stated the following on their earnings call: “on the enterprise side, there was also more budget scrutiny, especially from new categories, with longer adoption curves. Even when leaders understand the deep impact that Slack can have for them, the urgency, at the moment, favors short-term solutions to solve immediate problems. CIOs have a lot on their plates right now.”

Goldman Sachs equity research evaluated 50+ public SaaS companies and identified two interesting trends that tie back to what we’re seeing in our portfolio:

SaaS vendors relaxed payment and billing terms, primarily for end customers hit hardest by COVID-19 Vendors have also exhibited flexibility on contract lengths, allowing companies to move from multi-year contracts to single year. In an attempt to be well-positioned with customers for the future, this incremental flexibility— especially for customers in heavily impacted industries—should generate some goodwill, which will translate into less churn and higher net retention over the long-run. We called out a similar trend in our Q1 report, and it's interesting to see such customer-friendly policies continue.

CACs increased slightly in the quarter. The average CAC across the software sector increased primarily due to deceleration in ARR growth coupled with limited S&M increases. CACs moved up slightly for mid-market and enterprise companies, with only SMBs experiencing a slight QoQ decline. GS similarly believes we’ll continue seeing a slowdown in S&M spending primarily driven by a decline in travel.

5. Companies prioritized culture and individual engagement to keep morale high, and relied more heavily on OKRs to keep teams operating efficiently while at home

Maintaining company culture when operating in a remote-first environment was a key pain point for companies we met with in Q1. Over time, firms developed specific events and routines to promote culture and ensure employee wellness. These centered around increased time-off, virtual team events, accessibility to mental health resources, and promoting transparency across the org. Our portfolio company Transfix set a fantastic example here. The company “put in place employee engagement programs that have helped support four main pillars centered around: Health & Wellness, Celebrating Connections (internally and externally), Diversity & Inclusion and Learning & Development.” Building on this, we’ve called out a few additional examples below.

To promote connectivity, we have “each person call a random person in the company outside their normal orbit.”

“We introduced ‘Wellness Wednesday’ where employees can close off early and do meditation and yoga classes.”

“We have implemented monthly escape days, created a culture committee, and made company all-hands more engaging. We are also doing a lot more training for managers.”

“Extending half-day Fridays has been a morale booster without any corresponding drop off in productivity.”

CEOs’ key feedback to other leaders was around spending time with employees. The team at Transfix again shared: “It’s an important time to be over-communicating and investing in employees. Provide ways of being more connected to the mission of the company and to each other. There are many small, meaningful ways to do this.” Their sentiment was echoed across the portfolio:

“Go out of your way to do 1:1s to check in on how people are doing emotionally. It's very easy to just be "out of the loop" during this time.”

“We’ve found that openness and honesty—particularly during these challenging times—have engendered significant goodwill and reinforced the feeling that “we’re all in this together.”

In working to keep teams aligned on corporate goals, companies increased their reliance on OKRs and clearly defined KPIs. Not only was this seen to drive alignment, but also helped promote org-wide visibility:

“We have begun using OKRs for the first time to drive alignment across the company and definitely recommend them as a way to help engagement of employees who want to understand what other parts of the company are doing that they no longer see, and to understand how what they are doing directly affects top company priorities.”

Last, as we predicted in Q1, remote work is here to stay. 91% of survey participants stated an intention to continue to support remote work. For portfolio company Rocket.Chat, “WFH brought an opportunity to hire talent all over the world.”

While we believe there are benefits to company communication when employees are either all remote or all in-office, the transition to fully-remote will likely be a long one, with companies favoring a hybrid environment for now. Only 27% of respondents expect to be remote-first or fully distributed, and 9% expect to remain office-first.

Of all the insights, we were most surprised by shifts in IT spend over the last quarter, and are eager to see where startups decide to reinvest going forward. We’ll continue to watch closely as these trends evolve over the next few months...stay tuned for an update! In the meantime—we’d love to hear your reactions to these trends. Please reach out to us with any comments or questions over email or on Twitter: @jaisajnani, @psonsini, @alex_sharata; Learn more about us at https://www.nea.com/, @NEA.

***

Methodology: At NEA, we’re fortunate to have invested in a group of world class enterprise companies spanning stages and geographies. To quantify these trends and build on our Q1 research, we looked inward within the portfolio and shared a 10 question survey to our enterprise software companies in early September 2020. Here, we’ve presented the aggregated results.

Sources:

Bain & Company: Lockdowns Spike Spending on Collaboration and Software Tools -- https://www.bain.com/insights/lockdowns-spike-spending-on-collaboration-and-software-tools-snap-chart/

Bain & Company: The Pandemic Isn’t Boosting Cloud Spending -- https://www.bain.com/insights/the-pandemic-isnt-boosting-cloud-spending/

Goldman Sachs Equity Research: Americas Benchmarking Software -- Stock Recovery Reflects Long-Term Optimism in Software Post COVID

Goldman Sachs Equity Research: Future of Work: Collaboration and communication software August 2020 metrics

About the Authors