Blog

by Ann Bordetsky and Hunter WorlandMay 17, 2023

“Young, Poor and Looking to Invest?” is how The Wall Street Journal titled its first feature on the commission-free, fractional trading platform, Robinhood, in 2015 [1]. The headline encapsulated the simple but revolutionary belief behind the upstart company: age or assets should not impede participation in financial markets. Robinhood, in the company’s own words, was on a mission to ‘democratize finance for all.’

Robinhood’s S-1 outlined its mission to open finance for everyday people [2]

Robinhood was part of a wave of consumer fintech platforms that made financial services more accessible by lowering costs and removing barriers. Neobanks like Revolut, Acorns, SoFi, Chime, or Nubank democratized core banking services, as platforms like Wealthfront or Betterment for passive investing; Lemonade for consumer insurance; CashApp and Venmo for money transfers; Lofty for real estate ownership; Titan for managed portfolios; or Wise or Remitly for remittances.

Marketing from platforms Robinhood, Nu, and Wealthfront highlight their ‘democratic’ mission [3-5]

For Millennials, a generation that largely came of age during the Great Recession and its aftermath, these platforms met the moment. The distrust of large financial institutions combined with the advent of the smartphone enabled a business like Robinhood to scale from zero to ten million accounts in just five years [6].

However, the next generation of consumers, Gen Z, is coming of financial age with a different set of behaviors, challenges, and relationships with financial institutions. After all, their memories of the Great Recession are more likely to include Nickelodeon, Ripsticks, and Just Dance, rather than bank runs, unemployment, and bailouts:

Original TikTok videos: https://www.tiktok.com/t/ZTRcWcRSf/; https://www.tiktok.com/t/ZTR3BSF81/

If Millennials shaped the last fifteen years of consumer fintech, how will Gen Z shape the next fifteen? In our research, we explored how Zs engage with financial services – what products they use, what products they don’t, their wants, needs, and so on. We looked at a survey of 18 - 25-year-old retail investors, had conversations with founders and operators, and yes, even scrolled through personal finance TikTok and Instagram to uncover insights. As we dug deeper, one consistent theme emerged – Millennial fintech products democratized, Gen Z fintech platforms will socialize.

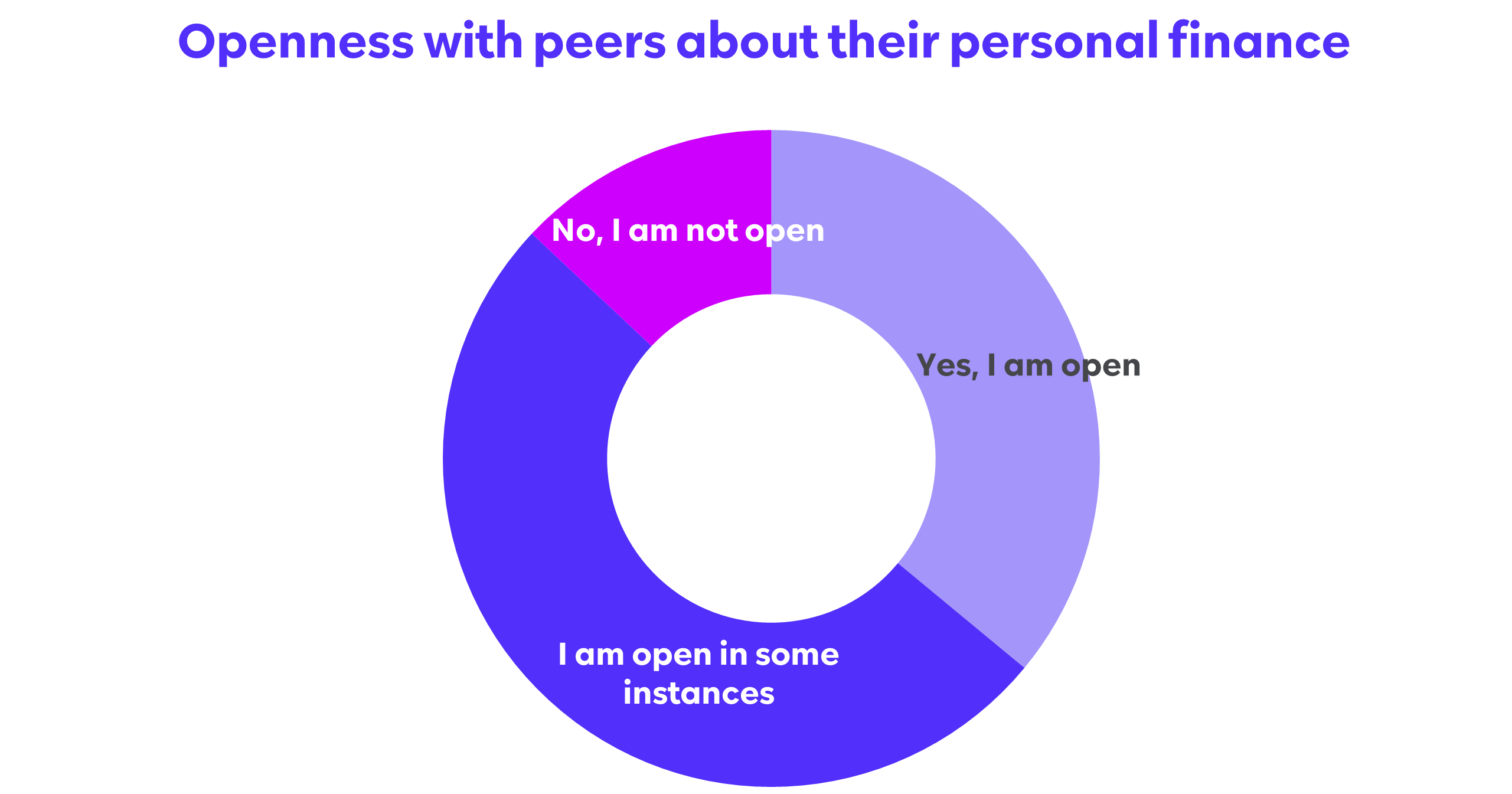

Personal finance, a traditionally private matter, no longer feels personal – at least to Gen Z. Over 90% of our respondents are totally or somewhat open about their finances with their peers:

We attribute this shift to two larger phenomena: financial accessibility and social media nativity.

Gen Z largely takes the once radical idea of democratized personal finance – radical only fifteen years ago – for granted. Take securities trading as an example. Platforms like Robinhood, which that eliminated fees and minimums, enabled fractional trading, and packaged servicesit all in a user-friendly mobile app have made it easy for Gen Z to invest their own capital – even if it’s only a few hundred dollars from a part-time job or a summer internship – and, in turn, learn investment fundamentals.

As a result, investing is no longer an esoteric, country club subject, but something more earthly. That accessibility is perhaps most obvious in trading, but applies to any financial category that the 2010s ‘democratized,’ like budgeting, credit, or savings.

The modern constellation of communication and media platforms from TikTok to iMessage have augmented the ability to socialize about finance. That augmented socialization happens in peer-to-peer channels, like a group text conversation about a jump in Tesla stock, and in more public spaces, like Discord channels on climate investing or an online community for Gen Zers filing taxes for the first time.

While some consumers from earlier generations have adapted to this behavior, the inclination to socialize among Gen Z – be it to share a stock pick or crowdsource whether to use TurboTax or H&R Block – is instinctual.

Social media has made Gen Z far more inclined to share, learn and seek out personal financial advice from peers, communities, and creators.

We believe there’s a matrix of different social layers that entrepreneurs can apply across the range of horizontal consumer fintech categories, from the trendy (crypto investing) to the mundane (fiiling taxes). The social layers we imagine are equally broad, applicable to any dimension of a product from its UX to data architecture. The permutations seem endless; we’ve highlighted just a few ways we think founders can meet the opportunity.

A saying on TikTok goes something like this: People see me spending money and think I’m rich… I’m not rich – I’m irresponsible!

This could be a generational maxim. Personal finance for the newly financially independent has always been difficult, but unique macro conditions have compound these difficulties.

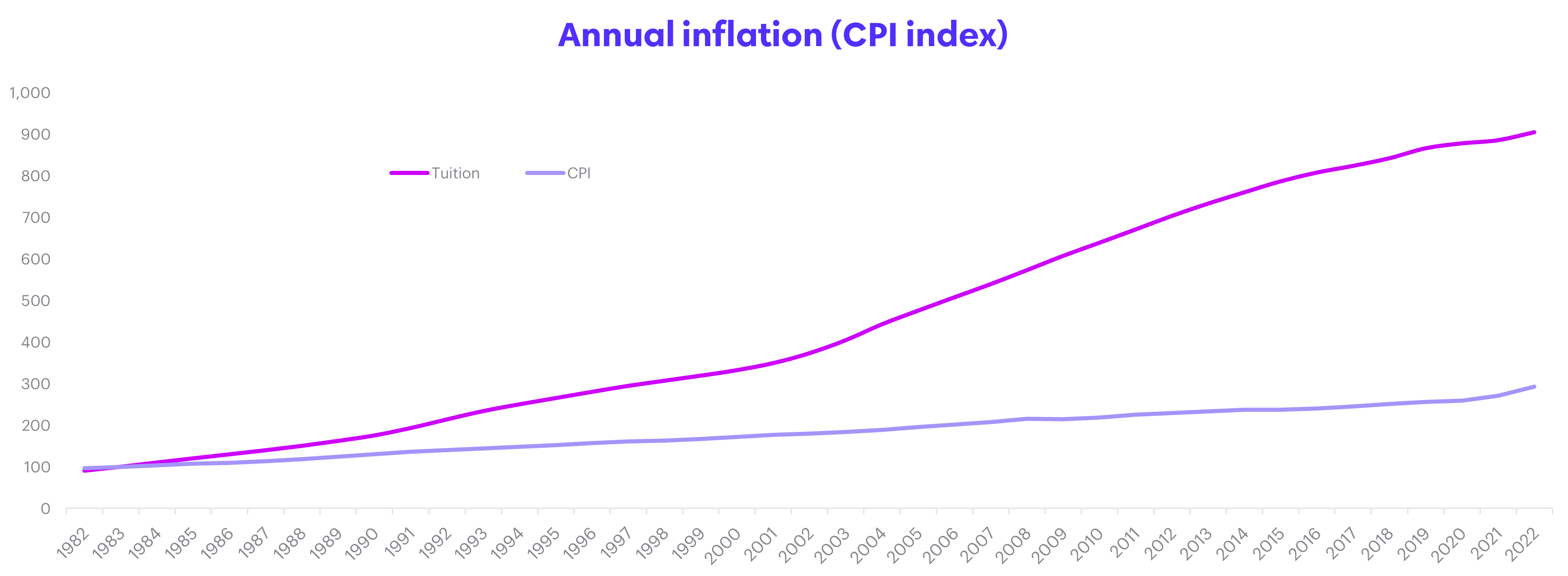

Developments in point-of-sales financing has enabled Gen Z to accumulate credit card debt faster than any prior generation. Rent in some big cities, where young people concentrate, has inflated as much as 30% last year alone [7]. Tuition, relative to a standard basket of goods, was expensive for Millennials; it is astronomical for Gen Z:

Tuition in the United States is more than twice as expensive than it was 20 years ago [8]

These barriers make financial security particularly elusive for our survey respondents. When asked about the greatest challenges preventing them from achieving financial comfort, they pointed to “learning to save money when everything is so expensive,” “fighting the urge to buy things without thinking,” and “having to be more disciplined with spending habits.”

In the face of these difficulties, Gen Zers have turned to peers on social media for personal finance guidance. TikTok, for instance, is littered with advice:

Original TikTok videos: https://www.tiktok.com/t/ZTR3BMth2/; https://www.tiktok.com/t/ZTR3BrvxN/; https://www.tiktok.com/t/ZTR3BRpbd/

We believe this demand for peer-to-peer wisdom and social benchmarking underlies a larger opportunity to socialize financial intelligence.

Today, personal finance tools are commonplace. Virtually every incumbent mobile banking app, from Chase to Bank of America to SoFi, has some kind of portal or content library. But the insights, recommendations, and guidance they offer are often arbitrary, outdated, static, or self-directed.

For consumer fintech applications like budgeting and savings, we believe entrepreneurs can socialize individual user data across relevant peer groups. These clusters could span from broad groups, like birth year cohorts, to the hyperlocal like a campus club, or a class of entry-level professionals at a specific employer. This kind of social data intelligence can offer users unique value by identifying anomalies among peers (e.g., a user spends a disproportionate amount on a given category), and dynamizing benchmarks to reflect the modern economy.

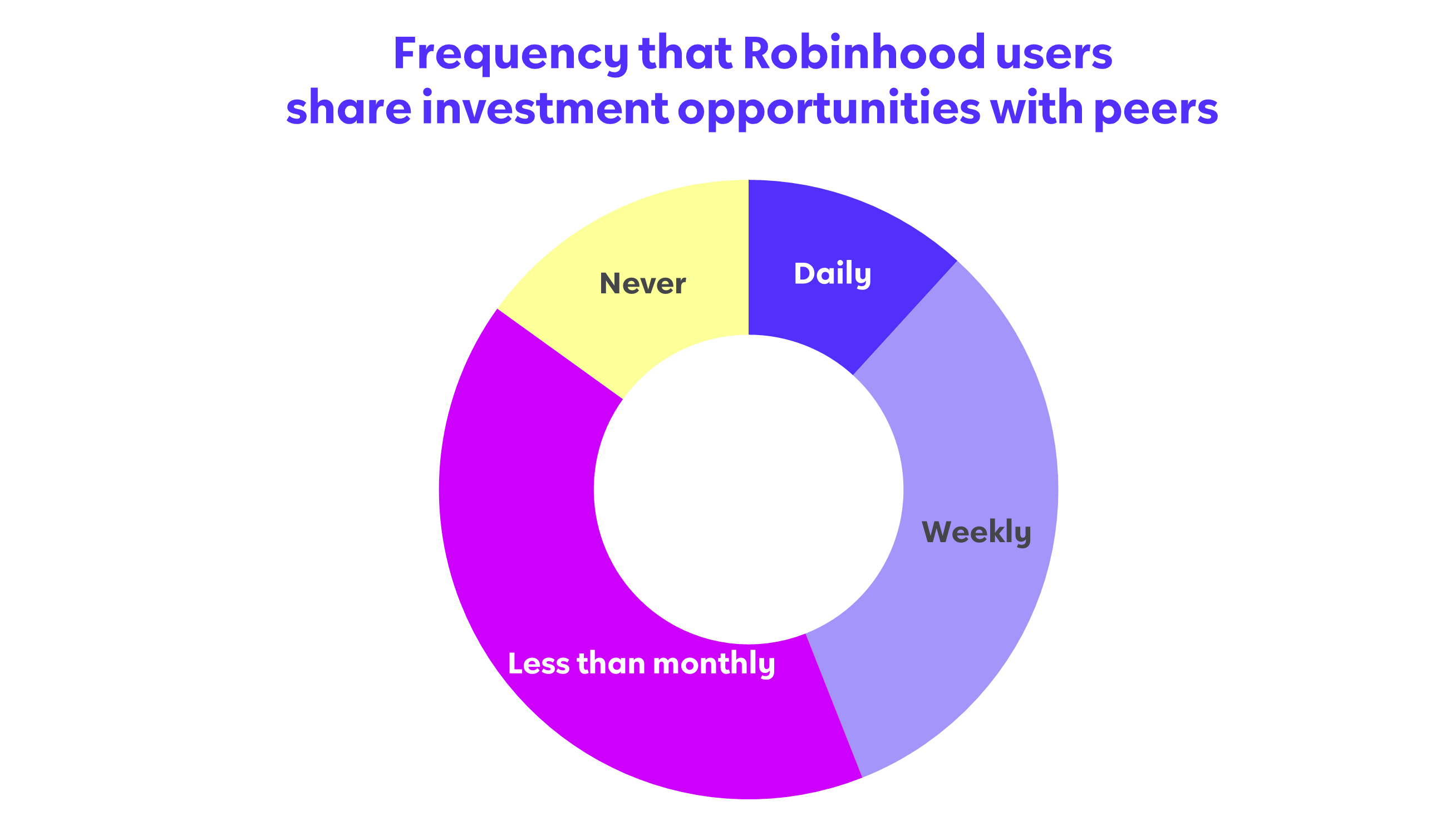

Gen Z investors are remarkably collaborative, conversational, and consultive – in other words, social. For example, of the survey respondents that use Robinhood, nearly 45% discuss investment opportunities at least weekly with their peers; another 34% share opportunities monthly. Less than 15% of survey respondents see investment details, such as how much money they invested, as private information that should not be shared with their network or community.

Peers, on or offline, are where Gen Z finds investment ideas, seeks portfolio advice, benchmarks performance, laments losses, or celebrates wins. These engagements transpire on incumbent messaging channels, like informal GroupMes or iMessage group texts between friends, and are littered with screenshots from personal Robinhood or Coinbase accounts.

We see an opportunity for founders to harness this organic behavior into a proper platform that reimagines groups rather than individuals as the atomic unit of investing.

On the surface, credit is probably the most difficult domain to socialize. Loans, debt and interest payments make for less exciting conversation than an investment in Tesla stock or a budget for a summer vacation.

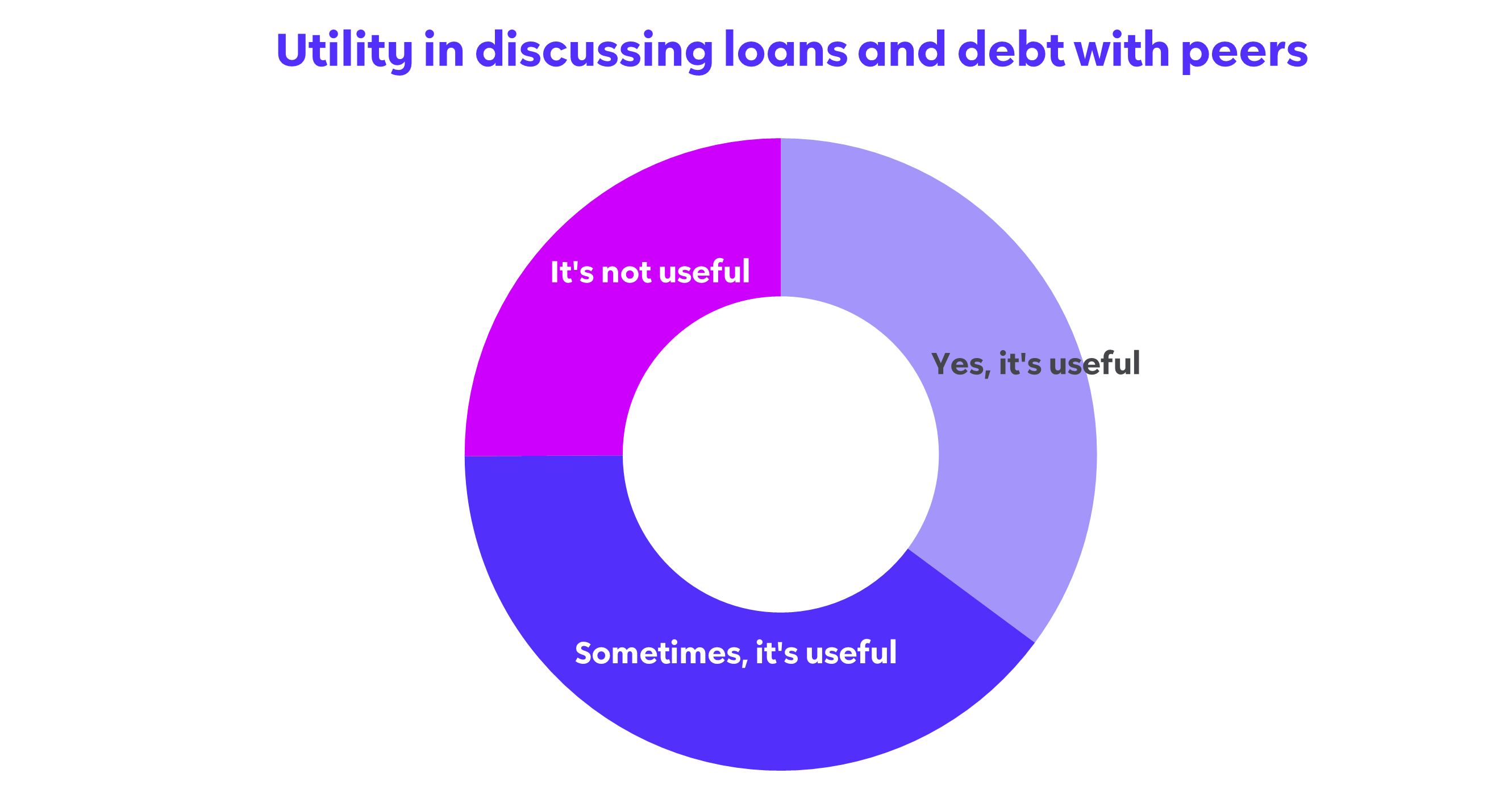

Accessing, managing, and servicing credit is typically stressful, but it is precisely that stress that makes social layers in this category so opportune. More than 75% of our survey respondents found it useful to discuss personal credit with their peers, pointing to the benefits of transparency, comparing processes and providers, and even just commiserating over challenges.

It’s no surprise then that over 80% of respondents consume social media content about dealing with loans or debt. Or that, hashtags like #debtfreejourney and #debtfree collectively have over a billion views on TikTok [9].

While the core functionality of credit will remain single-player, we see an opportunity for platforms that can combine the trust of regulated financial institutions with the social transparency, community, advice, collaboration, education, and even inspiration that users seek on social media.

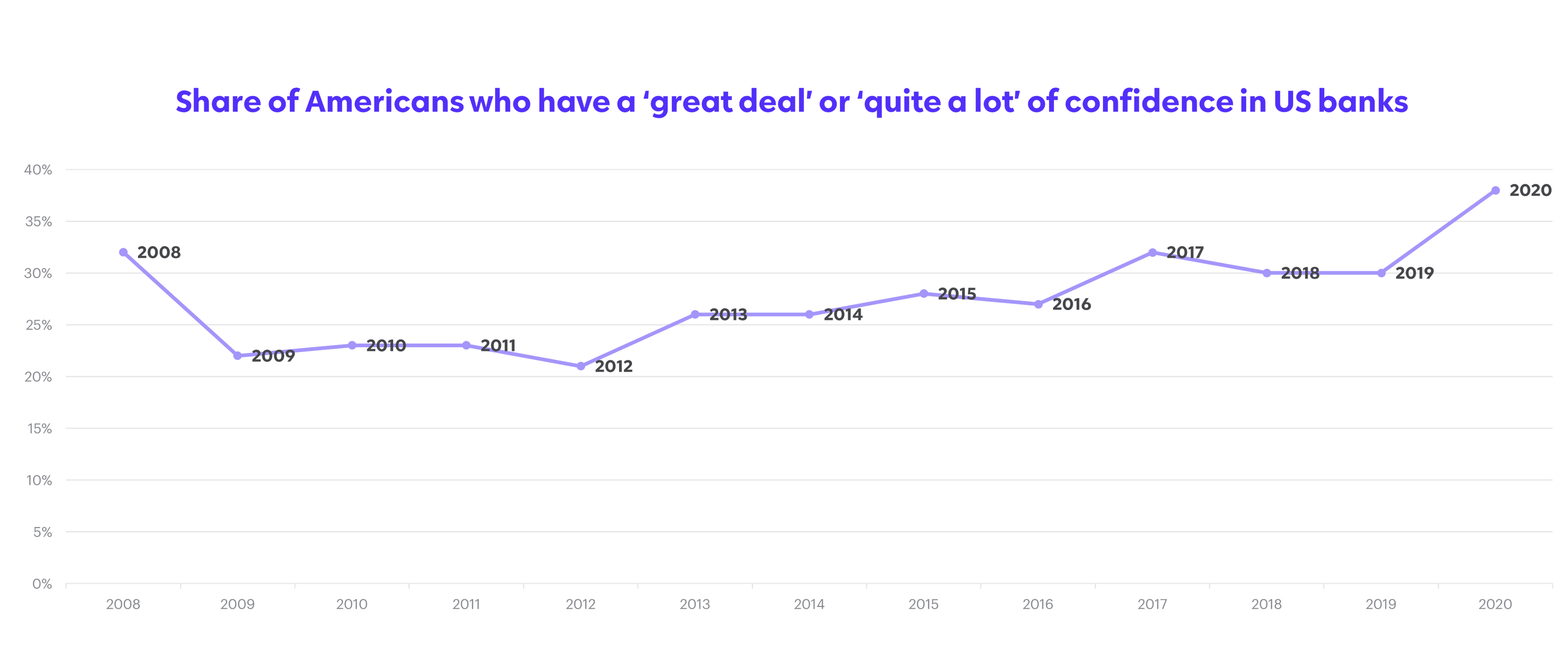

Millennials came of financial age during the nadir of consumer confidence in traditional financial institutions. It is no wonder they embraced alternatives like SoFi, Robinhood, or Chime for core financial services like investing, lending, and savings.

In 2020, consumer confidence in US banks finally rebounded from post-recession lows [10]

Not only has trust in large financial institutions rebounded, but more alternative forms of lending, investment, and banking have faltered in the current market downturn, hawkish macro environment, and crypto winter.

Gen Z startups in this space will not have the same luxury as their Millennial antecedents; we believe successful consumer fintech platforms will overinvest in establishing trust with their customers. We will look for markers like preemptive compliance and legal hires, proactive relationships with regulators, and disproportionate allocation of marketing spend towards communicating the business’ effective stewardship.

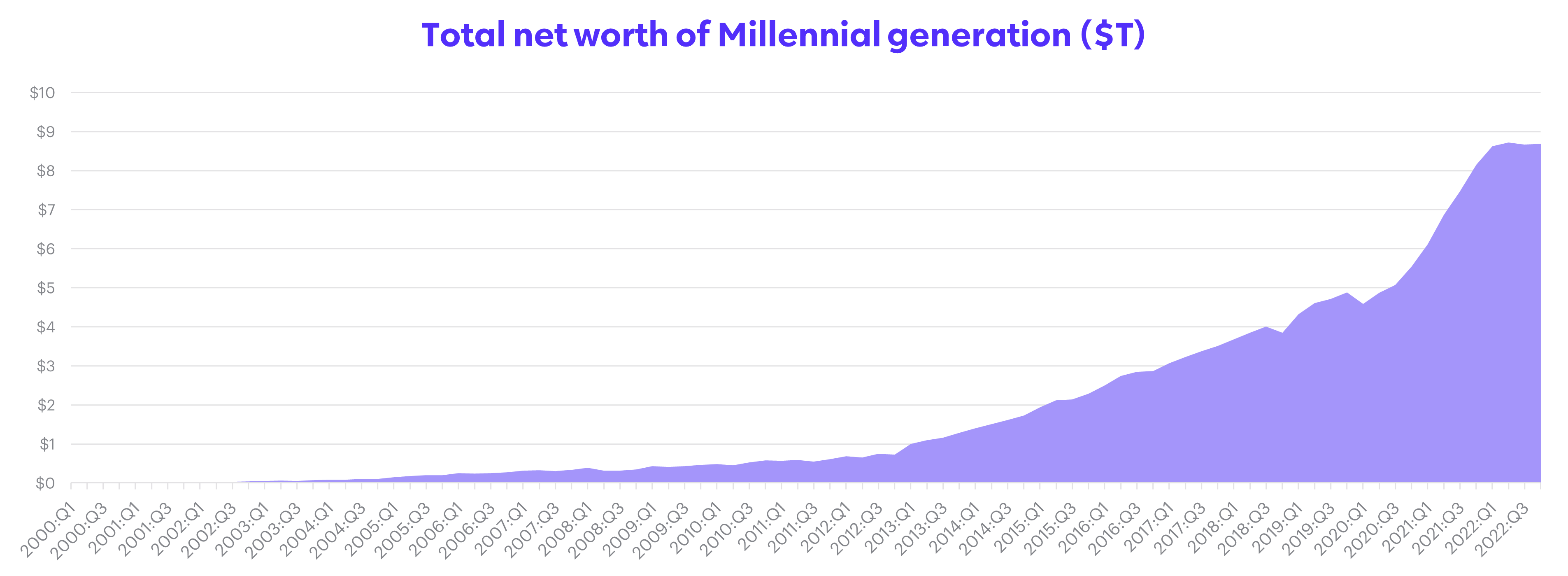

Personal finance data pegs the median annual earnings for working Gen Zers at just $32,500 [11], leaving little income for savings or investment products. But, with age and generational inheritance, these consumers will gradually accumulate more capital over time. Consider the cumulative net worth of American Millennials over the last two decades [12]:

We believe winners in this space will mature with their customers by offering products and user experiences that serve the long-term financial health of their customers, rather than their short term liquidity or portfolio returns. Successful founders will prioritize their customers’ potential lifetime value, even if it negatively impacts short term metrics, like daily engagement, minutes in app, or daily visits.

Privacy regulations like CCPA and GDPR, paired with Apple’s April 2021 privacy updates, have inflated customer acquisition costs. As Gen Z’s sheer youth already compresses initial ARPUs (recall the median generational salary), platforms in this category will likely not have the margin cushion to launch costly marketing campaigns (with all due respect to the E-Trade baby).

Founders can achieve more effective customer acquisition by harnessing virality across relevant social media communities. We will look for businesses that can engage a network of finfluencers, earn organic product reviews from relevant creators, migrate existing communities to their own platform, or effectively partner with content creators that generate viral promotional content.

The three most important takeaways from our research are:

The last fifteen years have been spent catering to Millennial behavior and needs. This has democratized most arenas of personal finance, and improved accessibility, usability, and affordability for the last generation of consumers.

We see an enormous opportunity over the next fifteen years to empower Gen Z financial services users with the tools to socialize – that is, to collaborate, knowledge share, commiserate, compare, contrast, advise, and form communities.

Winning businesses will bet big and early on consumer trust, prioritize long-term customer relationships over short-term engagement, and have no problem mobilizing users on social media to evangelize their product.

If you share our vision, let’s chat. Please reach us at: abordetsky@nea.com and hworland@nea.com

***

Notes and sources

We partnered with Attest to poll 200 consumers, aged 18 to 25, across the United States. For select questions, we ran a parallel survey with consumers aged 30 to 35. We ran these surveys in November 2022 and March 2023. To maximize data quality, Attest aggregates samples from hundreds of panels, communities, and suppliers and participating respondents received various incentives in connection with their participation.

All TikTok references are reflective of 2022 - 2023 trends.

The Wall Street Journal, “Young, Poor and Looking to Invest? Robinhood Is the App for That” (January, 2015).

Image from Robinhood, Form S-1 Registration Statement (filed with SEC on July 1, 2021).

Image from The Wall Street Journal, “Robinhood’s Biggest Business More Than Tripled Amid Trading Frenzy” (May 2021).

Image from Nu, Form S-1 Registration Statement (filed with SEC on November 1, 2021).

Image from Wealthfront.com/origin. Accessed online in April 2023.

Robinhood press release “Ten Million Thanks” (published on December 2019) Accessed online at https://blog.robinhood.com/new...

The New York Times, “Where Are Rents Rising the Most?” (February 2022).

U.S. Bureau of Labor Statistics, Consumer Price Index Database. Accessed online in April 2023.

Reflective of view count on Tiktok in April 2023.

Consumer confidence in United States banks is aggregated across Gallup’s annual ‘Confidence in Institutions’ surveys. Accessed on Gallup.com

GO Banking Rates, “How Much Gen Z Makes in Every State” (2023). Accessed online in April 2023 at https://www.gobankingrates.com...

The Federal Reserve, “Wealth by Generation.” Accessed online in April 2023.

The information provided in this blog post is for educational and informational purposes only and is not intended to be investment advice, or recommendation, or as an offer to sell or a solicitation of an offer to buy an interest in any fund or investment vehicle managed by NEA or any other NEA entity. New Enterprise Associates (NEA) is a registered investment adviser with the Securities and Exchange Commission (SEC). However, nothing in this post should be interpreted to suggest that the SEC has endorsed or approved the contents of this post. NEA has no obligation to update, modify, or amend the contents of this post nor to notify readers in the event that any information, opinion, forecast or estimate changes or subsequently becomes inaccurate or outdated. In addition, certain information contained herein has been obtained from third-party sources and has not been independently verified by NEA. The companies featured in this post are for illustrative purposes only, have been selected in order to provide an example of the types of investments made by NEA that fit the theme of this post and are not representative of all NEA portfolio companies. The company founders or executives or any other individuals featured or quoted in this post are not compensated, directly or indirectly, by NEA but may be founders or executives of portfolio companies NEA has invested in through funds managed by NEA and its affiliates. Any statements made by founders, investors, portfolio companies, or others in the post or on other third-party websites referencing this post are their own, and are not intended to be an endorsement of the investment advisory services offered by NEA.

NEA makes no assurance that investment results obtained historically can be obtained in the future, or that any investments managed by NEA will be profitable. To the extent the content in this post discusses hypotheticals, projections, or forecasts to illustrate a view, such views may not have been verified or adopted by NEA, nor has NEA tested the validity of the assumptions that underlie such opinions. Readers of the information contained herein should consult their own legal, tax, and financial advisers because the contents are not intended by NEA to be used as part of the investment decision making process related to any investment managed by NEA.